Spot Opportunities & Trade with Confidence. Open a Free Trading Account Today!

+91

Login for real-time prices and trading.

Here's what's available pre-login:

This pre-login view lets you study volatility behaviour before you trade on it.

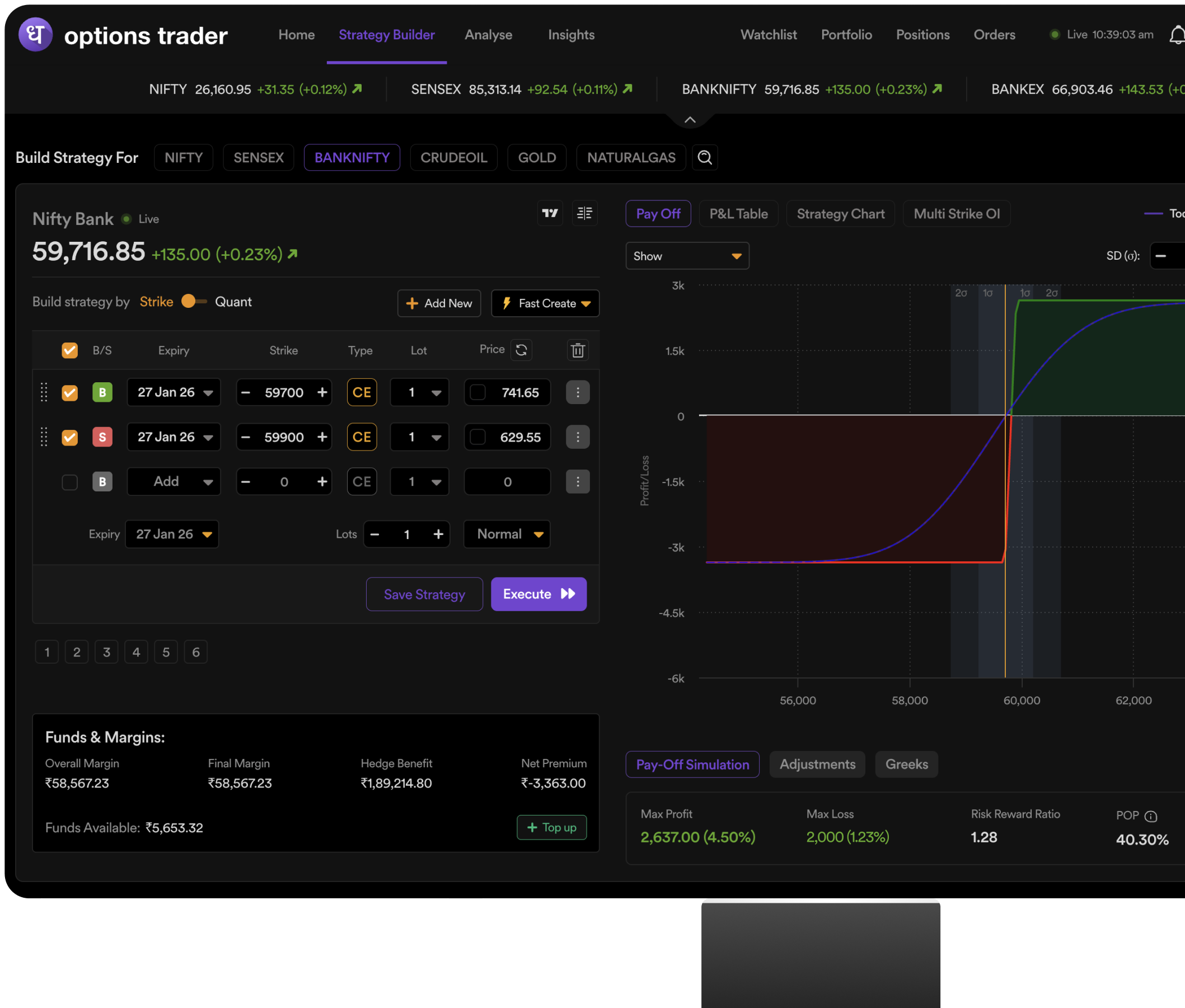

The IV chart shows NIFTY 50 with a 15-minute interval as a default for guest users. There is a single chart area with two distinct plots:

When viewed together, it makes it easy for you to view how the option premiums are responding to the actual price movements of the underlying asset in real-time market conditions.

Here's how you can read the following signals on the IV Chart:

As IV rises, option premiums also expand. This indicates that the market is factoring in a larger future price volatility, often because of fear, uncertainty or expectations of an upcoming event, such as RBI policy, budget announcements or geopolitical events. During expansion periods, option buyers have to pay higher premiums per trade, and sellers collect larger premiums.

When IV drops sharply, especially right after an event has passed, it's called an IV crush. Premiums collapse because the uncertainty that inflated them is gone. This hurts option buyers the most: even if the underlying moves in your favour, a sharp IV crush can erode most of the gain from your premium.

For broad market indices like NIFTY, price and IV often share an inverse relationship. When the underlying price falls sharply, panic sets in, and IV spikes. When the market slowly moves upward, IV tends to drift lower. Spotting this divergence helps you gauge broader market sentiment.

Implied volatility tends to mean-revert; i.e., it doesn't stay elevated or depressed indefinitely. The practical takeaway is that option sellers look to sell premium when IV is high (expecting it to cool off), and option buyers look to buy when IV is low (expecting it to expand).

Implied volatility is the market's expectation of how much an underlying asset will move over a future period. It is priced into option premiums by market participants, not derived from past price history, thus making it forward-looking.

Historical (realised) volatility, by contrast, measures actual past price movements. The distinction matters in practice as historical volatility tells you what happened, while implied volatility reflects what the market is pricing in for the period ahead.

IV isn't computed directly. It's back-solved: starting from an option's observed market price, an options pricing model (like Black-Scholes) is run in reverse to find the volatility input that would produce that price. In short, IV is the volatility the market is implying through what it's willing to pay.

You can use the chart controls for the following:

Use the search bar to pull up the IV chart for any index, F&O stock, or commodity, all accessible before login, but with 15-minute delayed data.

You can adjust the timeframe to view short-term volatility spikes or longer-term IV trends. Pre-login, you have access to the default 15-minute interval for all chart data.

After logging in with your Options Trader account, the following will be unlocked on the IV Chart:

Data delay is eliminated when you log in with an Options Trader account. IV and price data are updated in real time, which is crucial for intraday trading during major events or volatile sessions.

Once logged in, the chart will allow you to use 1-minute, 3-minute, 5-minute and 30-minute intervals as well as 15-minute intervals. All expiries and the F&O scrip universe are also unlocked.

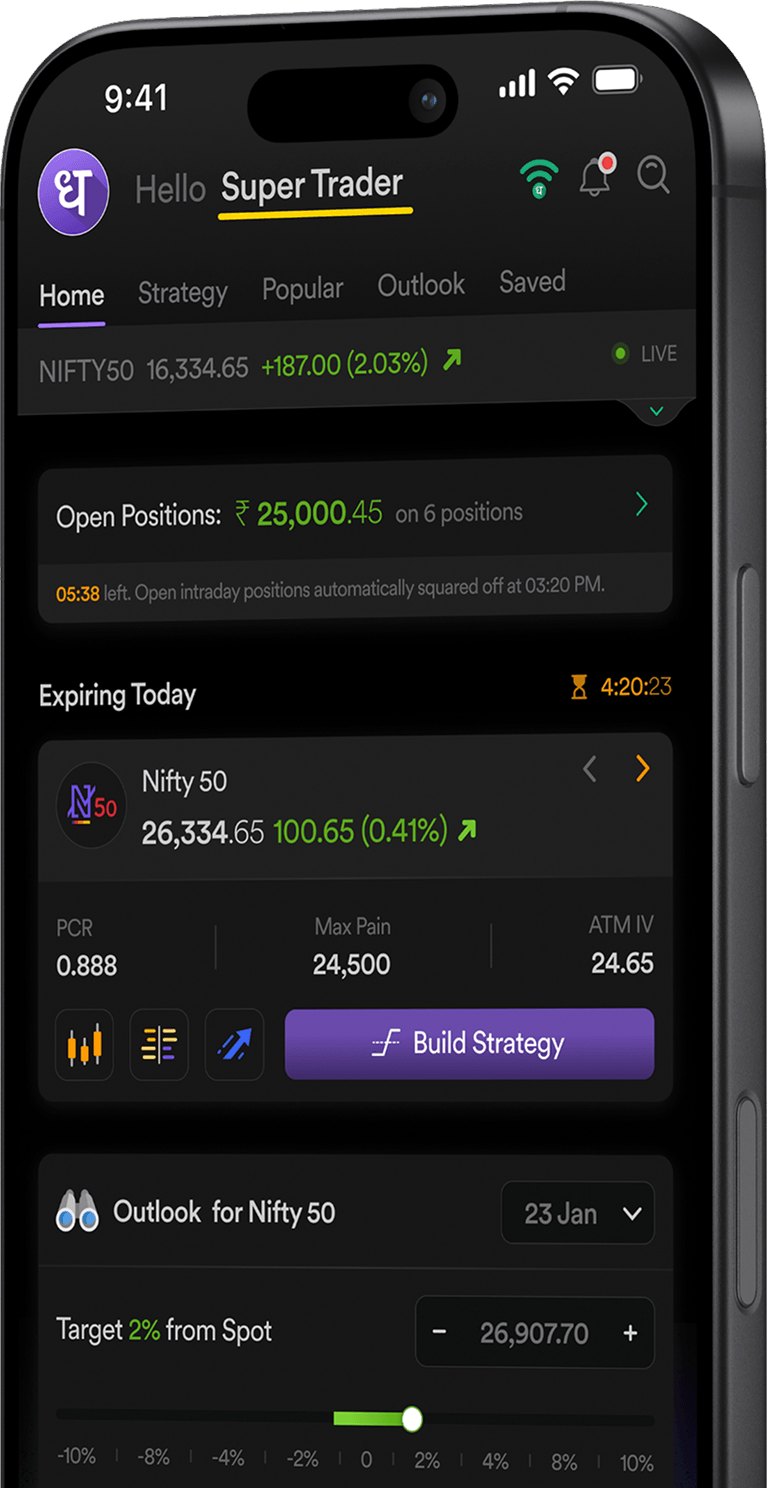

Options Trader is built specifically to assist F&O traders in their trading journeys. It offers:

IV level at entry affects the cost of every long option trade. Buying options when IV is elevated means paying a higher premium than the market may not sustain, i.e a correct directional call can still produce a loss if IV collapses after entry.

As per SEBI data, 9 out of 10 individual traders in the equity F&O segment incur net losses. Therefore, reviewing IV before sizing a position is the first step toward avoiding entry at inflated premiums.

Historical volatility is calculated from actual past price returns over a set period. Implied volatility is extracted from current option market prices and reflects where the market expects the underlying to move, not where it has moved. IV is forward-looking; historical volatility is backward-looking.